Millions of people are unemployed. Traffic lines at food banks stretch for many miles. All over the US hungry people show up hours before the food banks open. They want to make sure they will get food for them and their kids before supply runs out every day. We have nearly 170.000 Covid related deaths in the US. In Florida we have 570.000 people infected and over 9.000 people have died.

All these negative news but the market goes UP

You need to see it in order to believe. All the above are signs for a bad economy – and especially for a Real Estate market that needs to collapse, but the opposite is happening. I entered listings into the Multiple Listing System ( MLS ) last week. 3 minutes after I had pushed the “publish” button, I had my first showing request. And from there on it got crazy. Calls never stopped. I had 25 showings in the first 2 days and 6 offers within this time. I was wondering if I had maybe listed these properties for too little. Remember: I’m in this business since 1984 and I was quite sure I did a good research before I listed these properties. But I went back and checked again. Result: I was dead on with my asking prices. Even worse: I was on the upper bracket of comparable. This means my listings weren’t cheap.

All offers over asking price!

Yes: All the offers I received came back higher than the list price. Now I had to start investigating what was going on. I started calling the other Realtors who had sent these offers. Their response was all the same: There are nearly no ( comparable ) properties on the market. Extremely many sellers had withdrawn their listings because of the Pandemic. They few properties left sell like crazy. We are in a sellers market again. Since I have all the numbers from previous months, I immediately went back to check if my collegues were right. And yes they were.

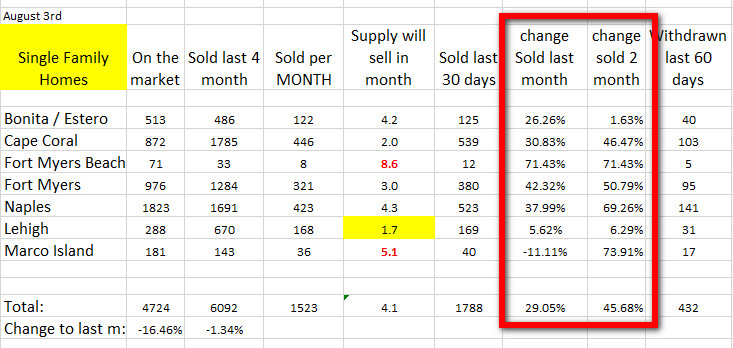

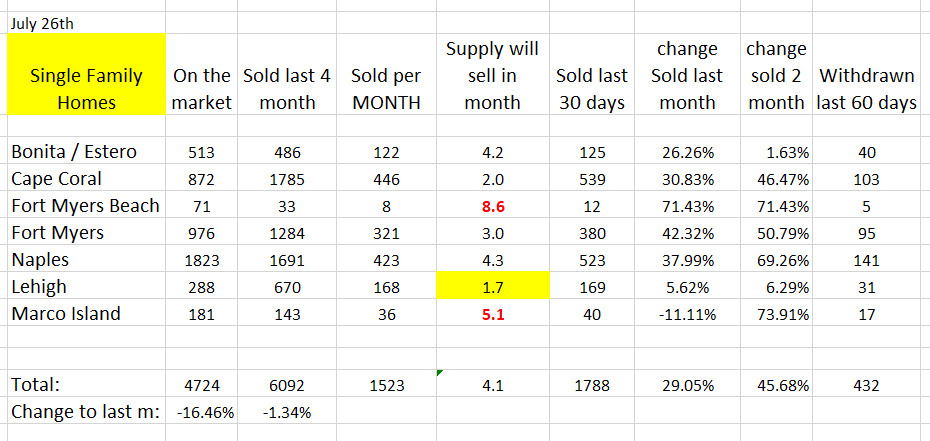

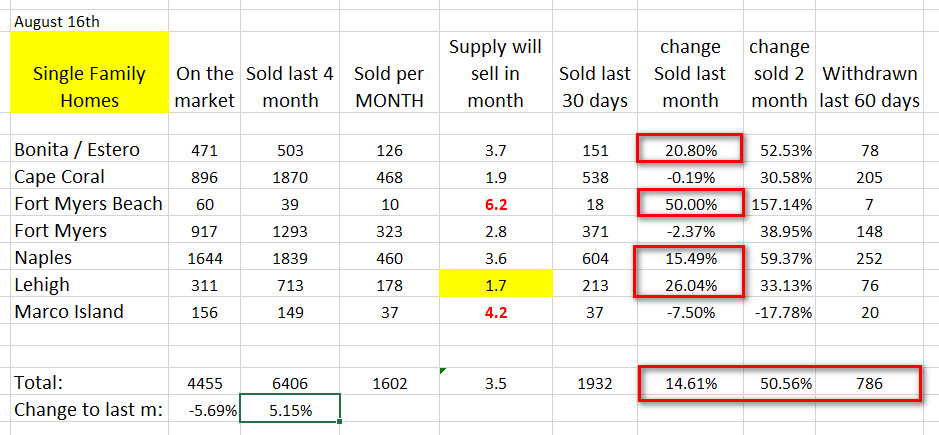

Facts from a few weeks ago: Single family homes

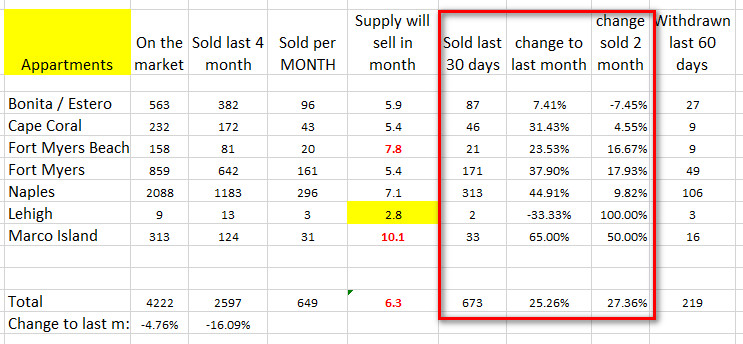

Compare it to the facts from August 16:

Let’s analyze it a bit:

Last month 432 property owners had withdrawn their listings – 3 weeks later this number went up 82% to 786 withdrawals. These people probably had the same info and knowledge than myself: With everything that happens in the world right now, the market had to collapse. Let’s pull the listing because I won’t get what I’m asking for. That’s common sense, but as you can see: It’s wrong. Although Cape Coral looks like it only had a few less listings, once you look at the following map you will agree that this seriously looks like a sellers market:

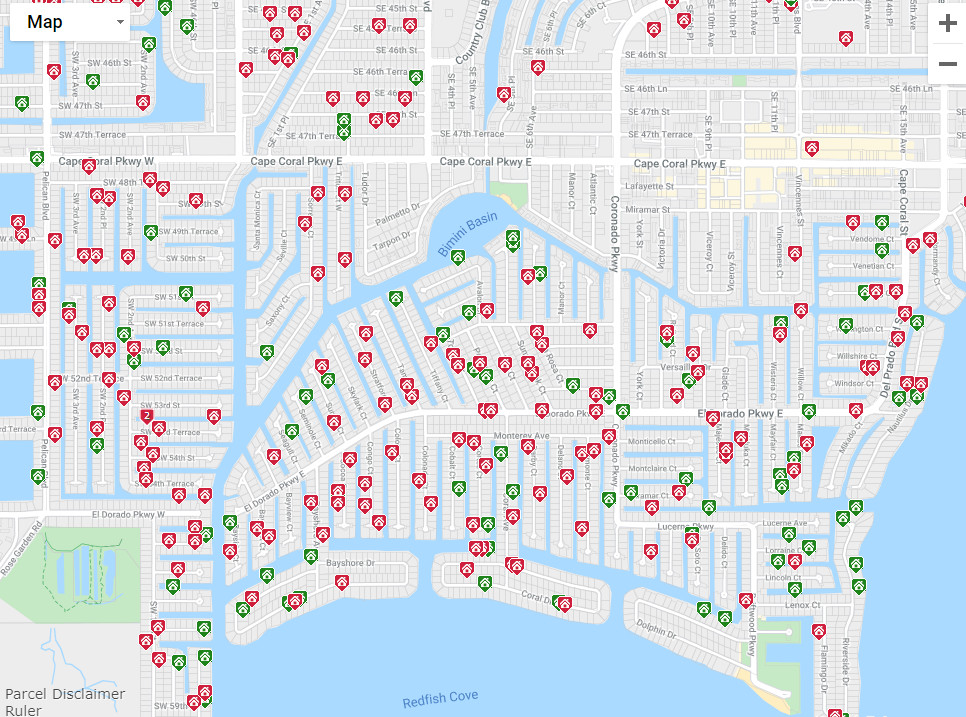

More RED than GREEN

This is an areal overview from today. Percentage wise there are way more red ( sold ) homes than green ( active ) homes. This picture shows single family homes active and sold within the last 120 days. So what does this mean for you?

As a buyer:

As a reader of my blog you know I suggested you should wait with your investment. Well: It looks like I was wrong. My conclusions haven’t been reflected by the market. The economy obviously has it’s own mind and once again the simple facts of Demand and Supply came to fruition. Less supply drives prices up. You should jump in. Sometimes it makes sense to neglect your feelings and senses and do the opposite. Lot’s of people do. In my blast blog I gave a few reasons why the market might not even collapse this time. Go back and read it. This time there is simply too much at stake. With this crisis there is no Government who can come and bail out single industries – at least not a collapsing Real Estate market. This could be the end of the Dollar. And believe me: Neither the current President nor the ( hopefully ) next President want’s this to happen. I start to believe the crash we were waiting for is not going to happen. A small correction maybe ( most probably ) but I was wrong before. I suggest you get in the game again – NOW!

As a seller:

Facts are facts. If your last name isn’t Trump you should believe what you see. Trust the experts. Trust the numbers. Look at the numbers and act accordingly. If you have a property you want to sell, then now is the time. You might be positively surprised what will happen once you list it. For all of you who can’t believe what you see I have good news: Do your own research. For this, I provide an easy tool right here on my website. Go to the Home Buyer link and go to Option 1:

- At the “Property Type” button click Residential

- Decide and click the cities ( areas ) you want to see results from ( i.e All Bonita Estero Areas )

- Click search

- On the next page you can see the results on the top

- Option 1 won’t let you check for properties that have been sold lately. If you want to get these info as well, go fill out your info for Option 2

Resume:

I’m long enough in business to honestly tell you if I made a mistake. Well…. I didn’t really make a mistake, but I came to the wrong conclusions based on what was in front of me and I told you about it. The market had other ideas and it’s time to adjust. If you are a buyer my advise is to get in asap. If you are a seller, you are considered a lucky one. Pick a Realtor, get it listed and lean back. Your sale is right behind the corner. Good luck to all of you.